Are you thinking about starting a business, or have you recently started a new venture?

You certainly aren't alone. In fact, 543,000 small businesses are started in the United States every month.

That's the good news. Less good: half won't make it until year 5.

The biggest challenge you're likely to face is not having access to the money you need to fully execute your business plan.

Think of your business like a video game: you don't want to play Super Mario Brothers with only one Mario. You want 5 "lives" because somewhere along the way, you're going to press the wrong button. Money for your business doesn't guarantee success, but having access to "do-overs" certainly makes it more likely.

The biggest tragedy to all this:

There's plenty of money out there for startup business loans.

You just may not know all the rocks to look under. Let's look at 15 ways you can access money for your new business.

Special Note: If you have a credit score of 700 or greater, just about the best start up business loans program we've seen offers up to $150,000 at rates from 7-10%. You may inquire about this program by clicking here.

New Business Loans from the SBA

Like any government program, Small Business Administration (SBA) Loans sound great in theory (let's make sure small business owners can get money) but the execution of the program is a total joke and a waste of everybody's time.

Of the 15 industries reported as getting the most SBA funding in the past decade, only 1 in 200 business owners in those industries managed to borrow a cent from the SBA.

With that being said, if you are one of the lucky few who is likely to qualify for SBA funding, and you have months (yes, months) to spare both waiting for your loan and making a giant business plan to appease an underwriter, these loans are sometimes worth the hassle as the rates are substantially lower than for any other new business loans a small business owner is likely to qualify for.

There are 3 types of SBA loans that a startup might be able to obtain, and they are:

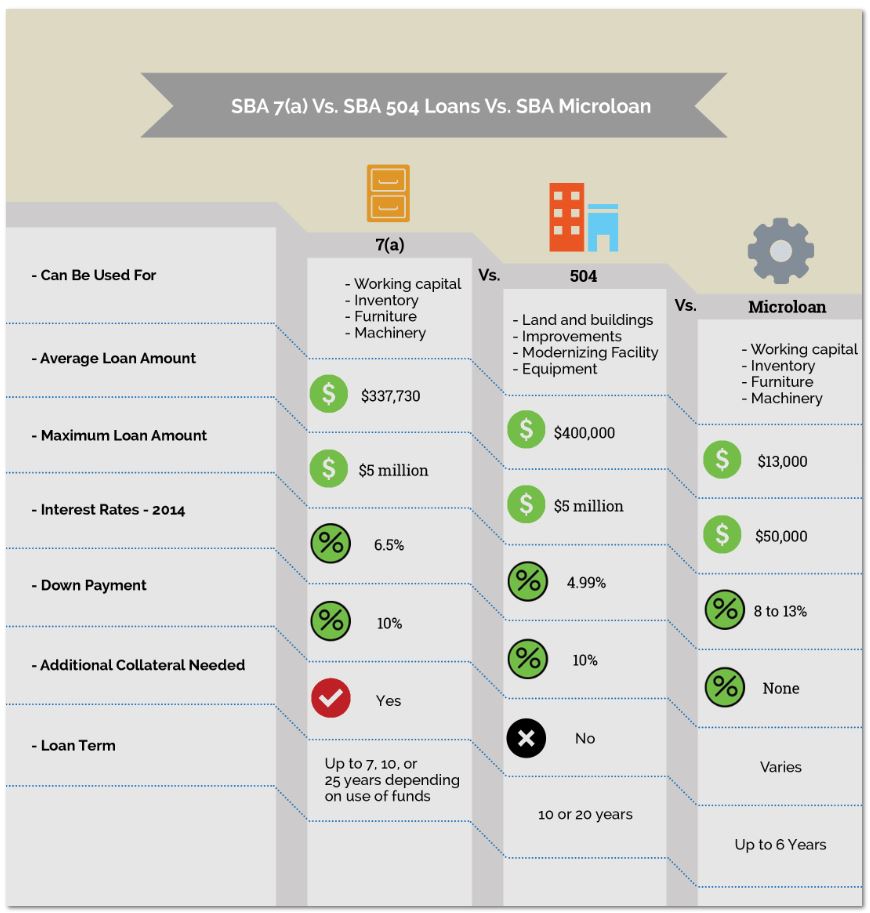

#1 - The SBA 7(A) Loan for Startups

The SBA 7(A) loan is a loan available to both existing businesses and startups. This loan may be used for real estate, equipment, or working capital. Here are the particulars:

- Loan amounts up to $5 million, but the average loan amount is $337,730

- Loan terms of up to 7 years for working capital, 10 years for equipment, 25 years for real estate

- The loan needs to be secured by collateral (usually your personal residence)

- A personal guarantee is required of all owners with 20% or greater ownership

- There will be a "blanket lien" placed on all assets of owners, both business and personal

- A 10% down payment will be required

The SBA loan 7(A) is just about the cheapest financing option for startups. Interest rates are very low, with rates set at a base rate plus a markup of 2.25 to 2.75 percent. The base rate can be either the prime rate, the London Interbank Prime plus 3%, or an SBA peg rate. As of September 2014 the total rate for an SBA 7(A) loan ranged from 6.25 percent to 7%. 7(A) loans are generally variable-rate.

The only problem with the 7(A) program is that very few business owners are actually able to qualify - roughly 85% of SBA loan requests are denied. You'll need great personal credit, lots of assets, and plenty of patience, since the SBA loan process can often take several months.

The SBA has a resource here to help you find local SBA lenders.

#2 - The SBA 504 Loan

Unlike the 7(A) loan, SBA's 504 loan program only allows your business to use funds for land, buildings, improvements to buildings, equipment, or modernization and/or construction of a building. The SBA 504 loan can also be used to purchase an existing business.

With the 504:

- Loan amounts up to $5 million, with terms of 10 or 20 years

- Your business must be creating 1 job for every $65,000 in funding ($100,000 if you're a manufacturer)

- The assets being acquired serve as collateral, but you will need to personally guarantee the loan

- You'll have to prove you couldn't get the funds elsewhere

- A 10% down payment will be required

Rates on the 504 are very low, with current rates of about 5%. The only problem with these loans is that very new businesses will qualify, and the process can take several months. A great resource for learning in depth about the 504 loan program is the 504 blog.

#3 - SBA Microloans

Not many people are aware of the SBA Microloan program, which provides loans through a network of intermediaries throughout the US. SBA microloans can be used for equipment, furniture, inventory, or working capital. The particulars:

- Loan amounts up to $50,000, but the average loan is around $13,000

- Collateral and personal guarantees are needed, but specific requirements vary by the intermediary

- Rates vary but are generally between 8 and 13 percent

- Repayment depends on analysis of your business, but the maximum term is six years

A big negative of the SBA Microloan program is that you'll be required to take business training and planning classes before even being considered for this loan. You'll also need to submit a business plan. The last downside is that it can take several months to go through the process.

Here is a list of all SBA approved microlenders.

#4 Startup Business Loans Program

If you have good personal credit, Smarter Finance USA works with a partner that can help you access up to $150,000 ($250,000 for medical startups) as a startup business.

The loan can be either a 5-year term or an open line of credit and features rates from 7 to 10%.

Here's what you'd need:

- Good personal credit (700+ credit score)

- No bankruptcies, foreclosures, or repossessions in the past 7 years

- No late payments in the last 2 years

- Note - having a history of past due accounts or any account settled for less than full balance will have a very negative impact on chances for approval.

If you have good credit, and would like to access startup business funding, please click here.

#5 P2P Lending for Startups

You may have seen mentions in the news about peer-to-peer lending platforms, but many people think these loans are available only to consumers.

About 3.5% of P2P loans are made to small businesses. Most P2P lenders do not accept startups, but we have helped customers look at a P2P lending facilitator that will:

- Help you access from $50,000 to $500,000 over a term of 2 to 5 years

- Rates range from 9% to 21% "simple interest"

- You'll need a minimum 700 credit score, an additional source of income other than the business you're starting, and a minimum of $150,000 in liquid assets

If you qualify, this is one of the better deals available on the market for a new business to borrow money. As our mission is to be totally transparent about rates with our customers, it's common to hear borrowers exclaim that rates sound high.

The truth is, these are the rates if you just started your business, because about half of small businesses will fail in the first five years, so companies offering loans at 5% to startups wouldn't be in business for very long. If you'd like to explore P2P lending for your startup, we can help.

#6 - Raise Funds With a Sale-Leaseback of Equipment

Some new business owners we talk to end up owning a lot of vehicles or machinery going into the business. Most of them are unaware that you can use the equity in that equipment to fund a business.

With a sale-leaseback you can receive up to 40% of the value of your equipment and pay it back over 2-5 years.

Bonus: since the money you receive is collateralized by stuff that can be taken if you don't make your payments, you can qualify for this loan with bad credit and $50 in the bank.

Also, since the transaction is structured as a lease, you typically get to write off the entire payments as operating expenses.

Rates on sale-leasebacks aren't low, but assuming you are going to make some profits with your new business, the tax savings offset a huge portion of the finance charges.

We've found that for customers in high tax brackets with good credit, after accounting for the tax savings rates on sale leasebacks are often pretty low.

#7 - Friends and Family Loans

So, this one is obvious, but what's not so obvious: how to facilitate it.

Borrowing from friends and family can be a mess if you don't have a third party coordinate the transaction - many people are awful record keepers, and quite honestly will forget to send payments on time - which can lead to big problems.

Another big problem - if the loan is to include interest, most people cannot accurately amortize loan payments - which can really lead to issues down the line.

There are some companies who for a reasonable fee will take care of the administration of privately organized lending. Here are a few to check out:

All three of these companies are inexpensive, with setup fees ranging from $0 to $200 depending on the options you need, and monthly administration fees ranging from $0 to $35 depending on the complxity of your loan.

#8 Run up Your Credit Cards

The website you're reading right now? Financed with good old fashioned plastic. Believe it or not, if you've got big limits unused on your credit cards, that may be the cheapest financing available as a startup.

How so? Let's say you've got $100k in credit limits on your cards, and a zero balance. Just run them up 50%, do a balance transfer, pay 0% for the first 12 or 18 months. At the end of that period, transfer them back to the other card.

This strategy is a little bit risky, because if the credit card companies suddenly tighten and shrink your limits, you can get maxed out pretty quickly.

You may hear "gurus" tell you not to use your personal credit to fund your business.

There is some merit to that, but as a small business, and particularly as a startup, any loan you take on is going to be secured by a personal guarantee (unless it's backed by real estate).

#9 Equipment Leasing for Startup Companies

A significant amount of the time that new businesses need funding, a large portion of that funding will be used to purchase business equipment, such as computers, machines, vehicles, etc. Many business startups don't realize that the equipment can be leased.

Leasing equipment works like leasing a car: you make payments for 2-5 years, at the end of which you can keep the equipment after paying a predetermined residual (often 10% of the original price of the equipment, or sometimes just $1) or you can choose to return the equipment to the lender.

Leasing is often the best option for startup owners that need funds for equipment, because:

- Most of the time, startups will qualify for some sort of equipment financing

- Leasing is very tax-friendly - often times the tax savings from leasing offsets a large portion of the financing charges from equipment leasing

- By leasing, you conserve cash that you'll need to run your business

- Leasing can be much easier to qualify for than other startup loans

We help a lot of new business owners acquire equipment via leasing, and you can download our free guide to equipment leasing by clicking the green button above.

#10 - Borrow from Your (or Your Spouse's) 401k

If you're starting a business while you have other employment, or your spouse has employment, you could borrow funds from a 401k.

If you talk to your financial planner about different options for funding your business, this will often times be cited as the least popular option. The reason why: half of small businesses fail. Your new business is going to be awesome, I'm sure, but nobody who ever started a business expected it to fail.

The simple fact is, the 401k is your safety net. If you fail miserably at your business, but you've got a 401k, your retirement funds are still in place. This has become even more important over the past 20 years: people don't die as young as they use to - your retirement funds may have to last you 40 years if you're lucky.

With that being said, borrowing from your 401k is one of the lower rate options, especially since you're technically paying yourself back. Here are the basics of borrowing from your 401k:

- You can borrow up to $50,000 or half of your plan balance, whichever is lower

- There is no credit check, and the money is technically "interest free" since it's paid back into your own fund

- The loan can be paid back over a period of up to 5 years.

One huge drawback to 401k loans - if you or your spouse leaves the job where the 401k is held, the loan usually becomes due immediately within 60 days.

#11 - Borrow Against Life Insurance

If you own a universal, variable, or whole life insurance policy, you can borrow against the cash value of it, typically up to 90 percent, at low(er) interest rates - typically 6 to 9 percent.

However, taxation rules and other things regarding borrowing against life insurance are beyond the scope of this article. Before considering this option, it is a good idea to run it by your accountant.

#12 - Fund a Business With Hard Money Loans

If you happen to own real estate that has a lot of equity, you can borrow money against it through private lenders. As a general rule, you can borrow up to 65-75% of the value of a property using hard money. So, if you owned a property worth $100,000 free and clear, you could probably borrow $70,000 against it.

Hard money loans are one of the only loans you can acquire without a personal guarantee, since the real estate secures the transaction. Also, they are easy to get as long as you have the equity - nobody cares what your credit is or whether you have any income - if you don't pay the lender will just keep your real estate.

The downside to hard money - it's not a cheap loan. You'll pay from a large origination fee (often up to ten percent upfront), and then 12 to 21 percent interest.

If you're looking for a hard money loan, a directory here has several lenders listed nationwide.

#13 - Factoring

A big challenge for a lot of startups (and businesses in general) - when you get your first customers, depending on your industry, your customers may not intend to pay you right away. This is especially true if your startup is in the medical services space, where you may be waiting on payments from insurance companies or the government.

Another reality startups might not be ready for: if you are giving your customers 45 day terms, for example, you're not likely to really get paid in 45 days. Some of your customers will have accounts payable people whose job it is to make up stories and excuses to stretch out A/P for as long as they can get away with - why use their credit lines to borrow money when they can just string out their suppliers?

Many companies sell off those invoices - for 2-5% a month you can get paid immediately on a portion of the receivables (typically 90%), which isn't cheap, but will give you the cash you need to stay afloat. The advantage to factoring: it's based on your customers' time in business and credit, not yours, so virtually every company with outstanding invoices will be approved.

#14 - Purchase Order Financing

Very similar to factoring, purchase order financing can help companies that have received orders but lack the funds to actually fulfill the orders.

We talked to a startup owner once who made oil to lubricate guitar strings. Like most owners of startups, he was short on cash, and received a big order for many, many cases of his oil. The only problem? He needed money for the plastic bottles, the label, the actual goop that he used to manufacture the guitar oil, etc.

Like factoring, P.O. financing can sometimes be expensive, but if you don't have alternative (cheaper) sources to raise the funds you'll need to fulfill orders, PO financing is a good financing option to consider.

#15 Crowdfunding

I'm often surprised when I talk to small business owners how few outside the marketing and tech spaces have heard of crowdfunding platforms like Kickstarter.

Let's say you make the best barbeque sauce on the planet, and you want to turn your hobby into a real business, but you'd need $100,000 to do it. You could launch a Kickstarter campaign, allowing customers to buy barbeque sauce before it was made - and essentially have your customers fund the business.

Sound crazy? Here are some companies that have been successful doing just this to fund their businesses.