When you look online for box truck financing, the most common question is:

"Will I qualify?"

The interwebs, in all their glory, tell you approximately nothing about this key question that you'll need answered to start making some plans.

Want to know a secret?

Are you going to get the straight scoop online?

No way Jose -

We've got to get you to call...

PS - If you don't want to read all this, or get bored, just click here and get a quick quote for rates to finance your box truck.

And, the rates? You want to know that too?

I mean, we can't just go and tell you what the rates are (not the real ones anyway) ....

..anyone in the equipment financing business would ask ....

Au contraire mon frere... (I think that's French for "Up Yours" ...)

To be fair, if you were to click around page 1 of your favorite search engine, you'll see some generous souls offering up sample payments...

...Which certainly seem reasonable...

...those fine fellows are being straight with you, right?

Just like this guy:

It would be totally nuts to give you real info before you're on the hook...

...so let's roll up breakfast and smoke it -

-because we're about to get real up in here.

[Well... we're going to show you if you qualify... and the rates too....]

1. Can You Finance a Box or Straight Truck With Good Credit?

Yep.

(Wasn't that easy?)

It's no secret - financing companies love it when you make your payments.

With good credit, you're in like Flynn, but there is a little bit of confusion about what "good credit" means.

Here's the ideal situation:

- Credit score 650+

- At least a few years credit history

- "Comp borrowing" - having made payments on a loan in the past few years on something with wheels

If you have all of those attributes, it's all good. Click here to get started.

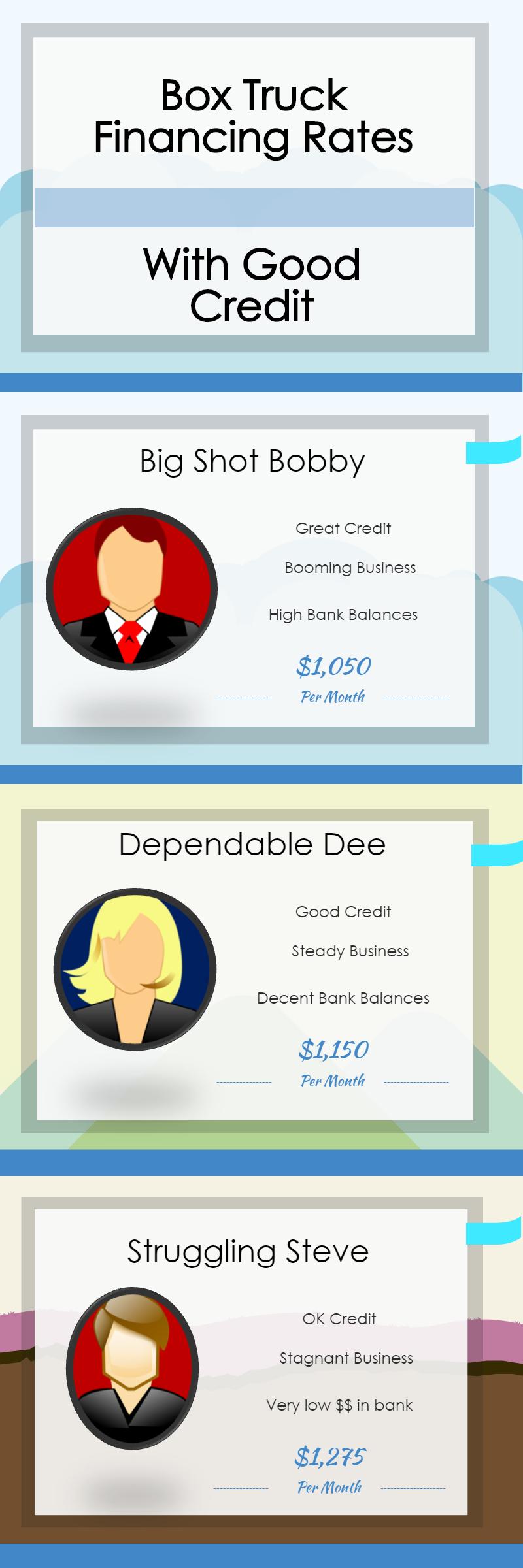

So what would your payments be?

Assuming 2 or more years in business (we'll go over startups in a second) here are some approximate numbers for when you finance a truck.

Note: We're going over payments assuming a $50,000 truck paid back over 5 years, and with no balloon payment at the end. Payments could be made cheaper with a lease - but you'd owe money at the end of the payments if you wanted to keep the truck.

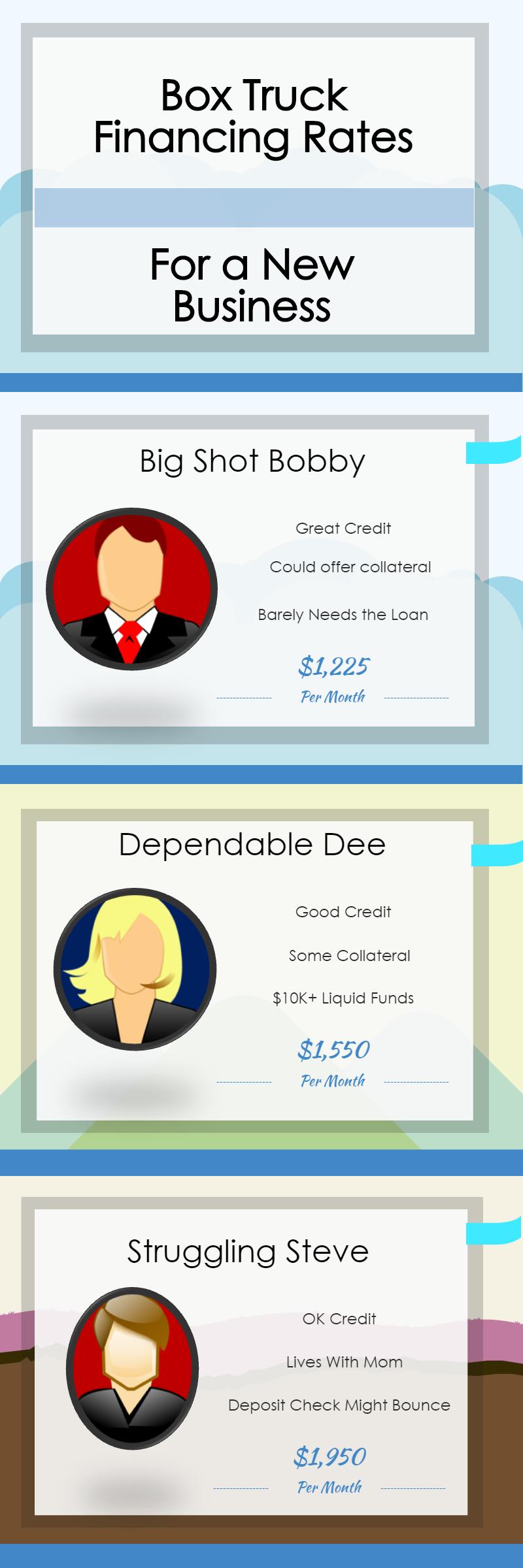

Now, if you're just getting business started, payments will be a lot higher.

(Here's where we get a little crazy.....truth telling and all...)

With good credit (or a strong cosigner) new businesses can usually get the equipment they need, but payments offered will make it seem like you were a bad credit risk or something.

Here's the deal:

Let's look at payments for our $50k box truck purchase again, assuming decent credit...

...but this time let's assume your business is just getting started.

Payments are high for startups, but as you can see if you've got good credit there's usually no problem in being approved.

To get approved, just get started here

As credit gets uglier, you have to be more creative to score financing.... but there are several more ways to get the financing you need for your business, such as...

2. Cash flow based equipment financing

Plenty of very viable businesses exist that are not candidates for low-rate financing, but have enough revenues that they can still qualify.

The model for cash-flow based financing is very simple:

Minimum Monthly Revenues = Equipment Cost

What this means is if you are buying a $50,000 truck, and your business does $50,000 or more in monthly revenues (as shown on your bank statements) in most cases you will qualify.

The typical payments on a $50k vehicle with a cash flow based model are around $2,275 based on a three-year term.

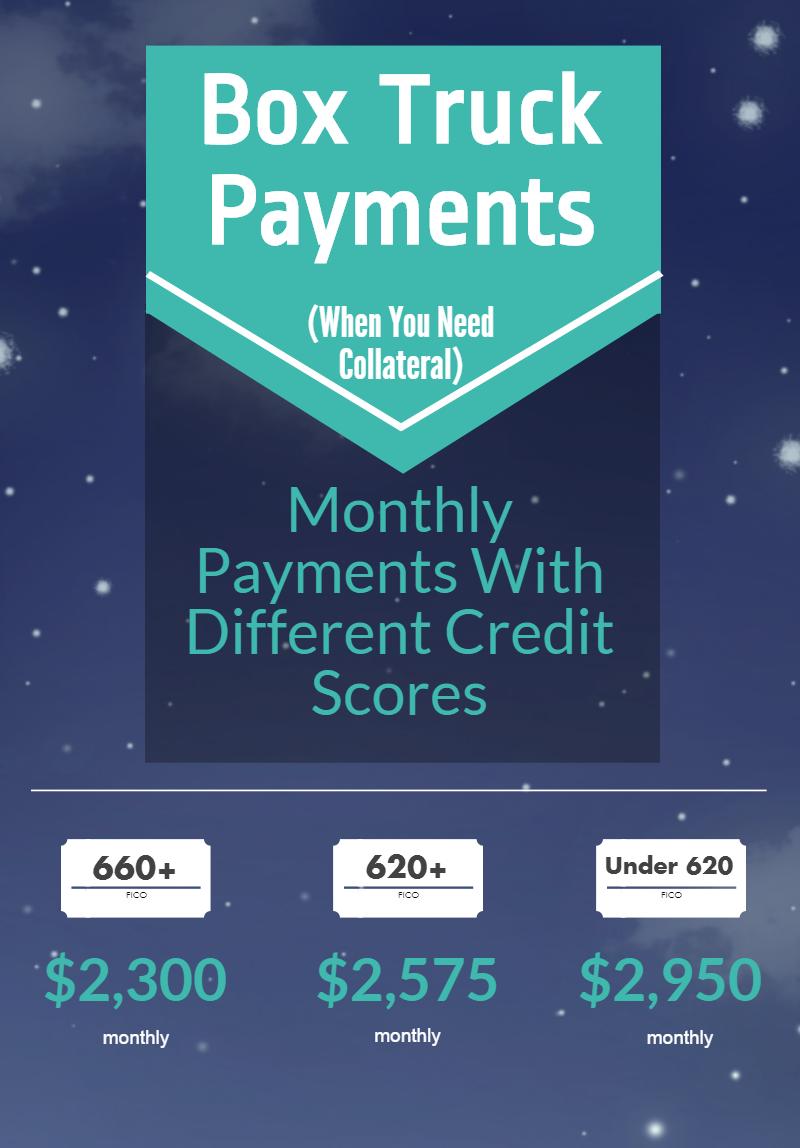

3. Bad Credit Box Truck Loans With Collateral

We often talk to business owners that have had "life" happen to them (and their credit trashed) in ways such as:

- Bankruptcy

- Struggling during the recession

- Divorce

- Medical problems

While the easy (cheaper) financing options may not be available after some of these events, collateral can fix almost anything.

Here's what you would need:

Business equipment, vehicles, or real estate that have a liquidation value (the amount the equipment would sale for at an auction) at least equal to the cost of the equipment you're buying, virtually anyone can qualify.

The only deal breaker is if you are currently late on child support owed to somebody.

When a deal has to be structured around collateral, rates are higher, but they really depend on your credit score. Find out what your rates will be here.

Also, payments will be higher as collateral based deals can rarely be stretched longer than 36 months. Let's go back to our $50,000 purchase, but we'll look at a 36 month term.

What would your payments be?

Yes - those payments sound pretty high.

Why do you think nobody tells you the real payments?

Since you probably don't have time to waste being lied to (or want to be scammed) those are the real payments no matter who you use when you've got some uglies in your credit file.

If you've got it pretty rough credit-wise, but don't have collateral, there are still ways.

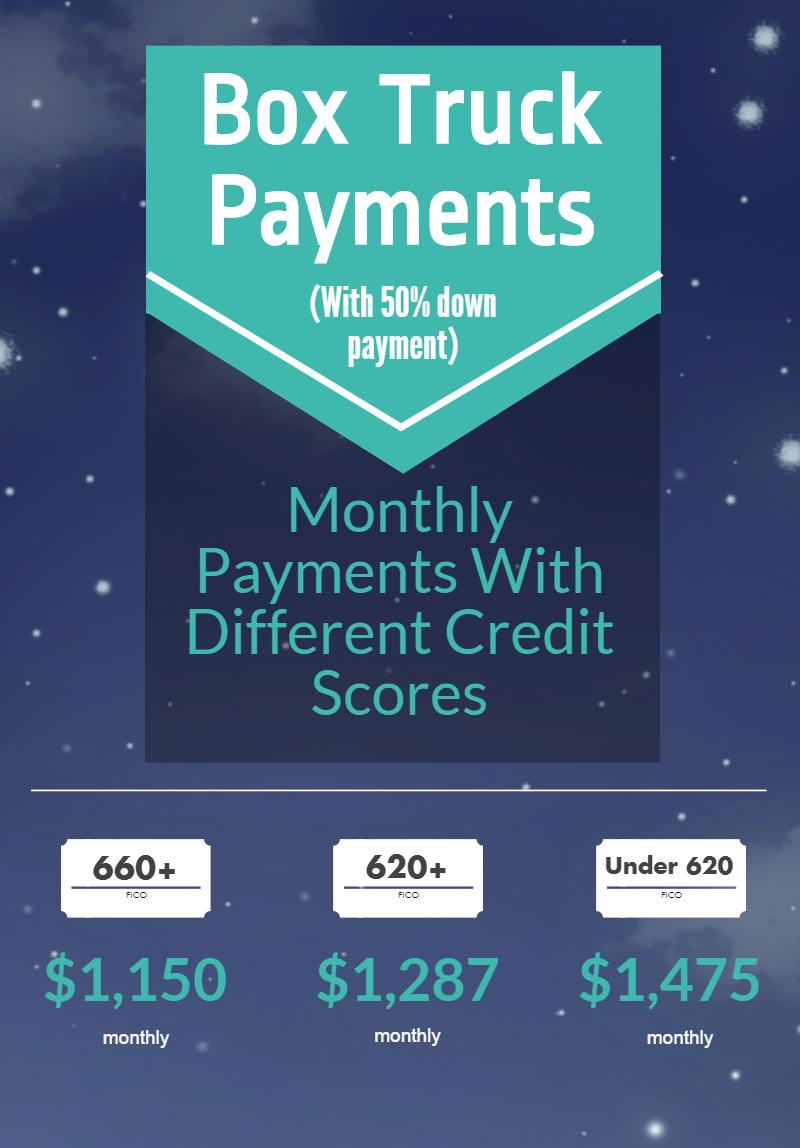

4. Bad Credit Box Truck Leasing With Big Down Payments

The good thing about box trucks (or any business equipment that has tires) is that they hold their values pretty well.

In most cases, if you stop making payments, the lender can recover about half of what you paid for the truck.

(They end up auctioning the truck, and then have to pay repo, storage and other costs).

If you have a 50% down payment, that works in 99% of cases.

(Not for deadbeat dads, though).

Payments are exactly the same on a dollar-for-dollar basis as what we just went over for collateral-based solutions, except since you're borrowing 1/2 the amount, payments are 50% lower:

PS - We often get asked, "Can you try to get the down payment lower?" ...

..and when the deal requires 50% the answer is always "no."

5. Story Financing

If you don't fit in any of the above categories...

.... but there's a solid business case to be made to lending to you...

... if your credit score is 550 or above and you have two or more years in business, story financing might work for you.

What "story financing" means is that there isn't a strict "model" -

Story lenders look for some strength to justify the deal, whether a down payment (but not always 50%) or collateral (but not always 100%) or some other method - and payments will be somewhere in the middle between all the other formats we just discussed.

Note - "story lenders" can be pretty loose, but nobody lends on total garbage.

If you have a credit score below 600, zero down payment, no collateral, and under $1,000 to your name, at least one of those issues has to be fixed before anyone will consider financing your purchase.

Ready to Rock?

To get started, give us a call at (866) 631-9996 or click the picture below.