Financing EV Chargers for Business: A Practical Guide

Electric Vehicle (EV) chargers are becoming more common – and it’s happening fast. They serve as the power source for electric vehicles, which are...

If you're trying to get the information you need about commercial truck financing you may be having some difficulty.

The big problem in the truck financing industry - some people that run financing companies learned early on in their career that if you come right out and say to people what the financing will really cost...

They will hang up on you.

It's better just to lie to you about the rates and payments - once we check your credit we can just make up some BS excuse why the costs are going to be higher than what you were first told.

Of course, by the time you've sent in your credit application, you've already picked out your truck and the dealer is going to be pissed if you don't get it financed pronto.

That's pretty lame, right?

Exclusive Bonus: To quickly learn your payments on a commercial truck, download the free guide to payments on commercial truck loans and leases.

People that call us generally want to know the answers to two basic questions:

1. Down payment: how much will I need to finance a commercial truck?

2. Payments: how much will they be?

There are more questions than that, obviously, but these are the most important ones that we find customers tend to ask about financing a truck.

Here's the deal - if you can't get straight answers to these two basic questions, you can't make plans on what you'll need to allocate for your business.

This is a big deal - it's not like you're buying some $19.99 potato peeler off of the TV - making the wrong decisions on your truck purchase can affect your livelihood.

Get an honest quote about what your rates may be

With that being said, let's talk about how to go about financing a commercial truck, and what the costs are likely to be.

In taking a look at what you'll need in order to finance a commercial truck, the first step is defining what you're actually looking at financing.

The first step is categorizing the truck, because depending on the type of truck, and the type of work it's used for, financing options could be a little bit different.

When people talk about a commercial truck, that could mean a couple of different kinds of truck, but usually they mean one of two types:

The rules are slightly different depending on what type of truck you are buying.

That's because some equipment finance sources will not touch long haul trucking deals, but other finance sources specialize in them.

Next:

What the truck will be used for...

... buying a semi tractor to be used with a dump trailer?

That's a vocational truck deal, not a transportation truck deal.

Just in case it wasn't confusing enough...

some companies will only finance trucks that are 10 years old or less,

others don't care,

and others claim they'll do trucks up to 15 years old...

...but ask them for rates on an older truck and they get all wishy-washy on you and whine if they can't find good "comps" for your collateral.

That's why... as we're going through all the different ways to figure out costs, I'll be throwing stuff at you like, "well, if the truck is old, payments might be this, but if it's new the payments might be that."

Of course... maybe you just want to get going on a quote. We can help you with that.

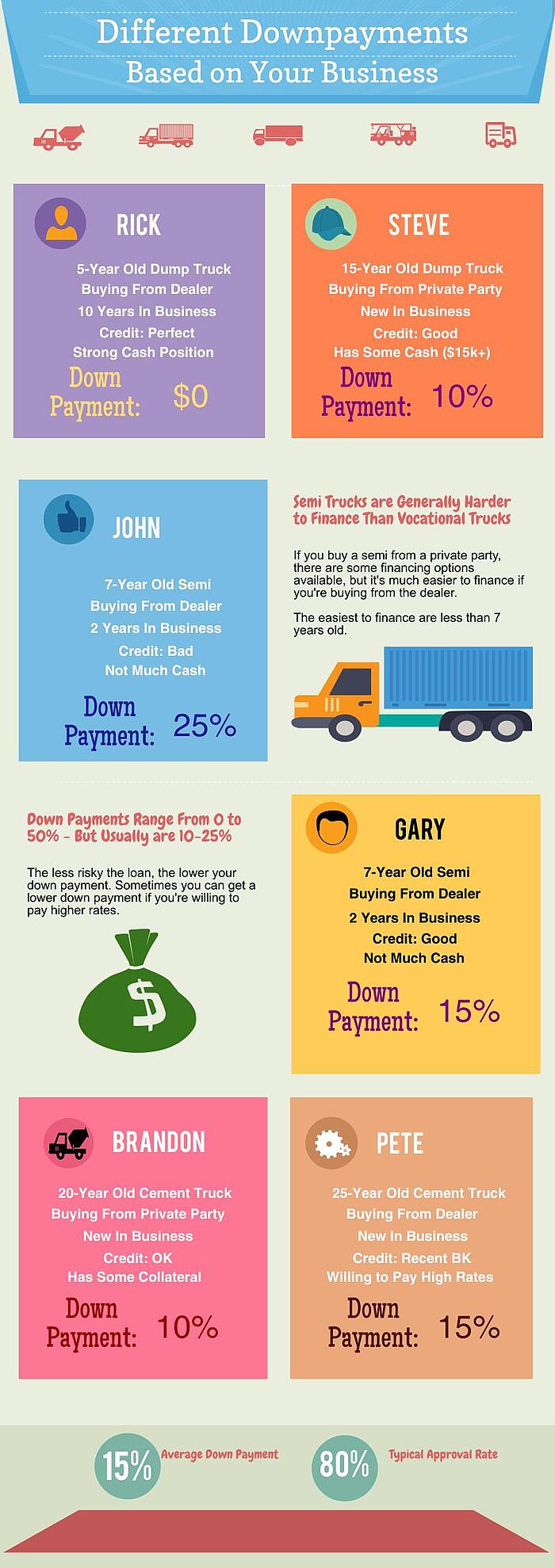

Down Payments for Commercial Truck Loans and Leases

Now that we're getting into the nitty-gritty, I'll give you some different scenarios.

There's all different ways to skin the truck financing cat, so these numbers won't always be 100% exact.

This will give you as close of a guess as is really possible based on different scenarios.

Vocational trucks are asier to finance than trucks that are used for long hauling.

Many equipment finance underwriters' guidelines say, "we'll finance just about anything in the world, unless it's a long-haul truck."

Many of the companies that do finance long haul truck companies won't work with owner-operators.

If you've been in business a while, have good cash flows, you're buying a newer truck, and you have reasonable credit, sometimes you won't really need a down other than the first payment.

As risk factors pile on, the amount of a down payment you'll need goes up.

These six basic risk factors can make your down payment higher:

Some of these have a bigger effect than others, but in most cases the down payment you'll need if you have any of these risk factors will range from 10% to 25%, though some programs will look for 50% down or collateral.

Find out which program is the best fit for you

It would be impossible to go through every situation, but here are a few scenarios to give you a better idea:

How much each of these things matters depends on how much risk they add, and there are some other considerations as well. We get a lot of questions about the different risk factors and why they matter, so let's go over them.

New owner operators generally have the toughest time getting approved for truck leasing.

Most financing companies won't consider owner operators that don't have 2 years in business. We've compiled a list of the best programs for new owner operators... but your situation will determine which program is best for you.

Before you've been through some of the challenges, you won't really know what to expect, which makes the risk of default higher.

It's certainly not impossible for owner operators to get financing, though.

(or there wouldn't be any such thing as an owner operator...)

Access financing programs for new owner operators

Here's are a few basic scenarios where a new owner operator can typically find financing without too much hassle:

There are zillions of other scenarios, but these are the basic things we run into.

When you get a commercial truck, credit score matters more in determining your payment than whether you'll qualify.

Still, bad credit can sometimes keep you from qualifying for commercial truck leasing.

If you've got bad credit and minimal down payment or collateral, it's going to be pretty hard to find someone who will finance you.

We talk to people with poor credit sometimes who ask if there's any way to get the down payment below 10%, and the truth is, that's usually not a very likely scenario.

If you have at least some money to put down, or some sort of collateral, you'll usually be able to lease a truck even with miserably bad credit - unless you've got one of the big 3 deal killers.

Can You Finance a Truck With Low Cash Reserves?

It depends. If you have reasonable credit, and aren't buying the oldest truck, there are some application-only underwriters - which means nobody is going to look at your bank statements.

Like everything else we've talked about though, it really depends on the situation.

Someone who isn't looking at your cash situation and is going to lend money to you has to compensate for that extra risk somehow - so they likely won't let you buy anywhere but from a dealer and usually won't let you buy an older truck.

Can You Finance an Older Vehicle?

As the age of the vehicle buying goes up, the number of underwriters interested in financing it goes down.

You'll usually have no problems financing something less than 10 years old, and while it's a little harder to finance a 15-year old vehicle, most of the time you can get those deals done.

After a vehicle hits 15 years, the number of underwriters willing to look at the deal drops by about 2/3. A lot of the time, the folks we're talking to don't understand why that is, but there's two reasons why funders get nervous about financing 20 year old equipment:

1. 20 year old equipment is going to break a lot more. If your truck is not working, neither are you, which makes it a lot harder to make your payments.

2. If you don't make your payments, the funder has to take your truck. It's a lot harder to sell a 20 year old truck than a 5 year old truck.

Note: We run into this issue all the time. New owner operators naturally want their first truck to be the cheapest they can get away with - so they'll have enough money to start their business safely.

In general, old equipment can be financed if we can make the deal make sense to an underwriter.

Lots of equipment finance companies say they finance trucks, but only if you have 3 or more vehicles. There's a lot less funders that will deal with a single owner-operator.

The reason for this - if you've got ten trucks and one of them breaks, you have ten percent of your fleet off the road. If you've got one truck and it breaks, you have zero income until the truck is fixed.

We can usually find a financing solution for you as an owner operator, but it's just not as easy as for fleet financing.

Truck financing is generally more difficult if you're not buying from a dealer - but like all situations, certainly not impossible. Roughly half of underwriters will only consider financing trucks when you buy them through a dealer.

What To Do Now?

Hopefully, this guide has given you a good overview of what it takes to qualify to finance a commercial truck. In most cases, we can find a way to get your truck financed, and we'll give you clear direction and no BS.

Ready to get financing on your next commercial truck?

Call us at (866) 631-9996 or click on the image below to get a quote.

Electric Vehicle (EV) chargers are becoming more common – and it’s happening fast. They serve as the power source for electric vehicles, which are...

The economic turmoil caused by the coronavirus pandemic has had an impact on small businesses everywhere. The Economic Injury Disaster Loan (EIDL)...

As a small business owner, you know you need access to capital…